[ad_1]

After taking over as chief executive of AstraZeneca in 2012, Pascal Soriot sent a team to a global life sciences conference to look for potential drug discovery partners. There were few interested takers.

“They were a bit of a joke,” says one veteran investor who attended the event. “They were going up to everyone, trying to do partnerships, but no one would listen.” AstraZeneca’s repeated failure to find new drugs to replace one-time money-spinners as patents expired was not enticing.

Seven years on, AstraZeneca has delivered one of the most striking turnrounds in global pharmaceuticals, producing a string of blockbuster cancer drugs that have catapulted it to the industry’s front ranks.

Potential partners “are not laughing now”, the investor says.

Last month AstraZeneca scored its latest success when Oxford university’s world-renowned vaccinology centre, the Jenner Institute, chose it as partner to develop and manufacture a potentially groundbreaking vaccine to fight the coronavirus pandemic. It picked the Cambridge-based drugs group despite its limited presence in the vaccine market compared with UK peer GlaxoSmithKline — which, as the world’s biggest vaccine manufacturer by sales, would have been the more obvious choice.

The decision is already paying off. Last week AstraZeneca said it had secured orders for at least 400m doses of the as yet unproven Covid-19 vaccine, as well as $1bn in funding from the US health department.

The Oxford deal represented a reversal of fortunes for the two companies, which carry the flag for Britain’s vaunted excellence in life sciences. Barely a year after being ridiculed at that conference, AstraZeneca was fighting for its survival against an opportunistic £55-a-share bid by US rival Pfizer — a battle that few investors thought it deserved to win after serial restructurings had failed to refill its drugs pipeline.

“Most investors were saying if they could get £57 or £58, we would take that — me included,” another institutional investor says.

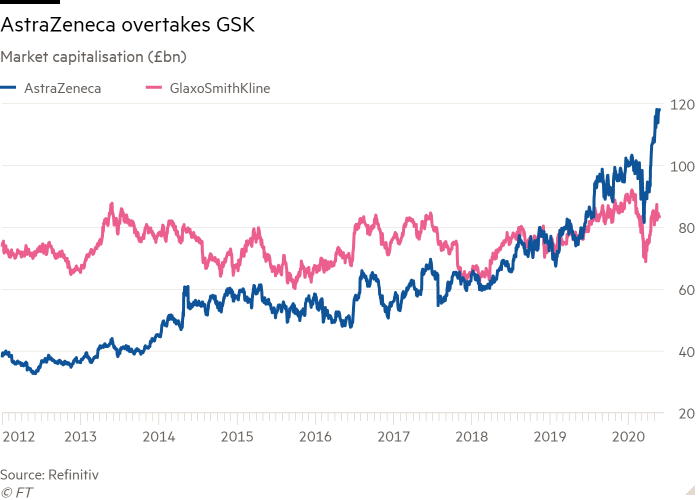

Now, having fought off Pfizer and built global leadership in groundbreaking oncology treatments, AstraZeneca is seen as the better bet to help manufacture and commercialise a new generation of vaccines. The partnership could also give the group a foothold in a near-$60bn a year market, which between now and 2024 is predicted to grow by about 7 per cent annually. The company’s shares now trade at almost £90, and it leads the FTSE 100 index of listed UK companies.

AstraZeneca’s success has put GSK under even more pressure to demonstrate that it can pull off a similarly durable R&D-led revival after years of failing to develop a cadre of new blockbuster medicines, despite a healthy number of regulatory approvals.

“AstraZeneca’s recent transformation has certainly given them a reputation for innovation,” says Adam Barker, pharmaceuticals analyst at Shore Capital. That puts them “at the forefront of collaborators’ minds when it comes to novel therapeutics”.

The Jenner Institute’s choice will not make or break either company. GSK has a partnership with rival Sanofi of France to develop a vaccine, as well as other initiatives to tackle the virus.

But it highlights the different paths taken by the two pharma giants over the past decade, and the scale of the challenge facing GSK’s chief executive Emma Walmsley as she attempts to reverse a decade of underperformance.

A month before Mr Soriot took over, AstraZeneca’s market value stood at £36.6bn, just over half of GSK’s £70.9bn. In recent weeks it has become the UK’s most valuable company by market capitalisation, at £118bn against GSK’s £83.4bn.

The companies’ contrasting approaches may also presage the changing fortunes of Britain’s pharmaceutical sector. “It is an interesting strategic move for AstraZeneca,” says one person involved in the vaccine partnership. “It is a commitment by them to play in this field. There will be a commercial opportunity in the global health threat that governments will want to pay money for.”

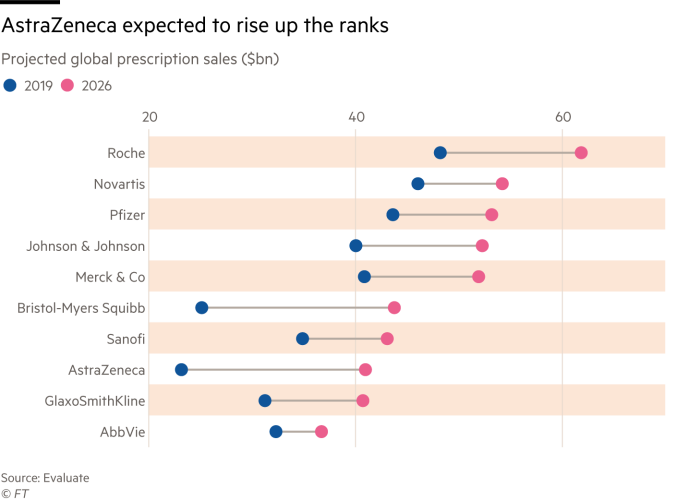

By 2022, AstraZeneca is expected to return to the ranks of the world’s top 10 pharma companies thanks to its new blockbuster drugs, according to data provider EvaluatePharma. By 2026, with annual drugs sales forecast to grow at roughly twice the rate of GSK’s, it should leapfrog its UK peer, barring any transformative acquisitions.

AZ’s top-selling oncology drugs

Tagrisso AstraZeneca’s best selling cancer drug is approved as a first treatment for certain types of advanced lung cancer. Approved by regulators in 2015, it notched up sales of $3.2bn last year. Sales are forecast to more than double by 2026 to $6.9bn. Recent trials suggest its use could be extended to prevent the return of the cancer in patients who have had tumours removed.

Imfinzi The immunotherapy drug is used to treat patients with certain bladder and lung cancers. It is forecast to be AstraZeneca’s second biggest seller, with sales forecast to rise from $1.5bn last year to $4.8bn by 2026, according to EvaluatePharma.

Lynparza The drug was first approved for the treatment of ovarian cancer at the end of 2014, and subsequently for breast and pancreatic cancers. It targets the genetic drivers of a patient’s disease. Jointly developed with Merck of the US, Lynparza was recently approved for certain types of prostate cancer. The drug delivered revenues of $1.2bn for AstraZeneca last year, with $4.7bn forecast by 2026.

Need for innovation

Drug discovery is a high-stakes enterprise. Billions can be spent on bringing a drug to market. Even then, fewer than 10 per cent succeed. Productivity in the industry has scarcely improved for years.

After a golden age in the 1990s, when drug approvals from the US Food and Drug Administration shot to record levels, innovation began to stall in the early 2000s. Bernard Munos, a former executive at US drugs group Eli Lilly, found that Big Pharma’s share in drug discoveries halved between the early 1980s and 2008, despite a sharp rise in spending on research and development.

The strategies pursued by many pharma groups — GSK and AstraZeneca included — of mergers and acquisitions to create industrial-scale R&D hubs had not worked. In the UK, the pain was compounded by the fact that both GSK and AstraZeneca were later than some peers to recognise the shift from chemical-based drugs — so-called small molecule medicines — into specialised biological treatments, which have been a more successful area for R&D.

“AstraZeneca and GSK had R&D that was not adapted to the new world,” says John Bowler, manager of Schroders Global Healthcare fund.

The sluggishness of Britain’s two big pharmaceuticals champions has had consequences for UK life sciences. British scientists, second only to the US in academic citations in the field, had been at the forefront of antibody research, for example, where drugs harness the body’s immune system to fight disease. “But the Americans capitalised on it,” Mr Bowler says.

Between 2010 and 2017 productivity in the pharmaceuticals sector fell by roughly a third, according to a 2018 study by manufacturing trade body Make UK. Gross value added — a measure of goods and services produced minus the inputs — had fallen back to 2001 levels by 2017.

As early as 2012 Britain’s big pharma companies were frustrating investors. GSK’s credibility was further damaged by bribery scandals in the US and China. But only AstraZeneca responded with a change in management, poaching Mr Soriot from Switzerland’s Roche as chief executive in late 2012.

With a scientist at the helm — one who also had experience of running Genentech, one of the most innovative biotech groups and a subsidiary of Roche — AstraZeneca began to prioritise the newest areas of science, while selling off all or a share in some drugs to raise funds for research and partnerships.

That strategy helped AstraZeneca traverse a difficult period, when it had to restock its pipeline. But some investors have raised questions about the transparency of the group’s reported results. Mr Soriot came under fire from investors for some of its accounting practices including over restructuring costs, while AstraZeneca has in the past derived substantial turnover from so-called “collaboration revenue” — income derived from royalties, drug disposals and partnerships.

“We sold out 18 months ago,” says Paul Major of BB Healthcare Trust. “The simple reason was opacity around deals they were doing. It made it very difficult to value the pipeline and . . . inflated core profitability.”

Cambridge move

Some of those concerns have since been alleviated by the return to growth of new product sales — driven by the string of blockbuster drug approvals that will deliver revenues for years to come. One of Mr Soriot’s earliest decisions was to focus on projects that had languished in the biologics division, formed as a result of the highly criticised $15bn acquisition of MedImmune in 2007.

But the masterstroke in 2016, say both analysts and investors, was the decision to shift AstraZeneca’s headquarters from Alderley Park in Cheshire to the heart of Britain’s life sciences hub in Cambridge, instantly changing the corporate atmosphere and offering immediate access to some of the world’s brightest researchers.

GSK, with its main research centre an hour’s drive away in the London commuter town of Stevenage, had chosen another route. Former chief executive Andrew Witty, an economics graduate who had risen through the commercial side, was a passionate defender of the company’s diversified toothpaste-to-vaccines model. He believed predictable revenues from the consumer health division would help to fund pharmaceuticals R&D, while also bolstering its ability to maintain the highly valued dividend.

In 2015, GSK swapped its oncology portfolio for the consumer and vaccines businesses of Novartis. In hindsight, suggests Phil Thomson, GSK head of global affairs, that strategy was flawed. “That [diversified] business model only works if the pharmaceuticals business is performing. Strengthening the pipeline had been the key need at GSK for years,” he says.

Oncology has since proven to be one of the most promising areas for novel drug development — and the driver behind AstraZeneca’s pipeline of treatments such as Tagrisso, the group’s flagship lung cancer treatment, and Lynparza, initially approved as an ovarian cancer drug.

Mr Soriot has admitted he had not counted on the oncology portfolio delivering as quickly as it did. “The fact we took a risk [on developing Lynparza] . . . and then it started moving, actually gave people hope and started building the belief that we had things in our pipeline and our research teams were better than people thought. It helped shape the culture,” Mr Soriot told the FT in an interview late last year.

Under Ms Walmsley, who took the helm in 2017, GSK is trying to rectify the mistakes of the past. The first step is the break-up of the company, due by 2022, into a consumer healthcare business and separate pharma and vaccines group. GSK aims to be a more specialised drugs company “focused on science related to the immune system, use of genetics and new technologies”.

Earlier this year Roger Connor, GSK’s head of vaccines, told the FT: “I don’t think there are many companies in the world that have the knowledge of the immune system that sits within GSK, and [we want to make sure that] in that ‘new GSK’ we completely exploit that scientific synergy between the groups.”

But some observers believe the pharma company will be small compared with other global players, and ripe for a takeover bid. To enhance its prospects, Ms Walmsley has made boosting oncology research a priority. Last year, GSK strengthened its cancer portfolio with the $5bn acquisition of US-based Tesaro and the number of oncology assets in its portfolio has doubled since 2018. However with 2019 oncology sales of £230m, it still significantly lags behind AstraZeneca’s $8.7bn.

Ms Walmsley, the former head of GSK’s consumer healthcare business, has tried to compensate for her lack of pharma expertise by surrounding herself with a team of science “rock stars”, in the words of Joe Walters, fund manager at Royal London Asset Management.

California based Hal Barron, head of R&D, was plucked from Google’s longevity start-up Calico, and had been chief medical officer at Genentech and Roche. Luke Miels, once Mr Soriot’s right-hand man at AstraZeneca, is GSK’s head of pharmaceuticals. His appointment sharpened the focus on pursuing only drugs with clear prospects of financial return after years in which its researchers had drifted off into “hobbyland”, as Ms Walmsley once told the FT.

That team has reassured investors. “Slowly but surely she is turning the group around,” says Mr Walters. Yet the team’s initial moves are now raising questions over GSK’s longer-term focus on the UK.

Dr Barron, who insisted he would remain in San Francisco to run GSK’s global R&D network, has led the deals hailed as crucial to transforming the group’s future pipeline.

As well as Tesaro, GSK has acquired a stake in West Coast-based consumer genetics testing company 23andMe and struck a five-year collaboration with the University of California San Francisco to establish a laboratory for Crispr technologies, which are used to edit genes.

Search for expertise

While the US remains the world’s biggest and most innovative market for drugs, there are concerns that GSK’s head of R&D could be missing opportunities closer to home. “All the insights are from California, when the smartest scientists might be on your doorstep in the UK,” says Dan Mahony, co-head of healthcare investments at asset manager Polar Capital.

“You can see with the partnerships Hal has entered into the centre of gravity is shifting outwards,” says Mr Bowler.

Investors point to the opportunities offered by the UK’s single-payer NHS that cares for all Britons and which could offer significant advantages when trialling new treatments. The data gathered by a single system could help accelerate development of drugs and the competitiveness of the UK industry, says one investor.

Mr Thomson says concerns about the company’s commitment to the UK are overstated, with £1bn a year invested in R&D in the country and Stevenage one of its two main global research centres. NHS data was “a very precious asset”, he says, but would require significant investment to exploit its full potential.

The NHS is starting to make connections between clinical trials and data and UK research infrastructure such as the biobank of health data, says Mr Thomson. “Making those connect in the UK to work in a viable way that industry can then access appropriately is absolutely the next step. You are seeing elements of that. But there needs to be more. If that happened, then the UK remains very attractive to us.”

Ultimately, GSK and AstraZeneca are likely to be agnostic about geography. “They’ll both . . . source [expertise] wherever is best. Of course, part of that is who or what you know already, perhaps why Hal has looked to the US,” says Mr Barker of Shore Capital.

The more immediate challenge is the heightened risk of political interference as public health and drug discovery become questions of national security. Both companies have committed substantial resources to fighting coronavirus. Investors understand that there will be little or no financial return in the near future from these efforts. But they may help to restore the reputation — and bargaining power — of an industry that has been vilified over the pricing of critical medicines that may have been developed with the support of taxpayer-funded research.

“Big Pharma has been under unremitting pressure for the last four years,” says Mr Major. “It is an opportunity for the industry to demonstrate its worth and value to society.”

Additional reporting by Donato Paolo Mancini

[ad_2]

Source link Google News